library(tibble)

library(dplyr)

library(ggplot2)

die_df <- tibble::tibble(

x = 1:6,

prob = rep(1 / 6, 6)

)

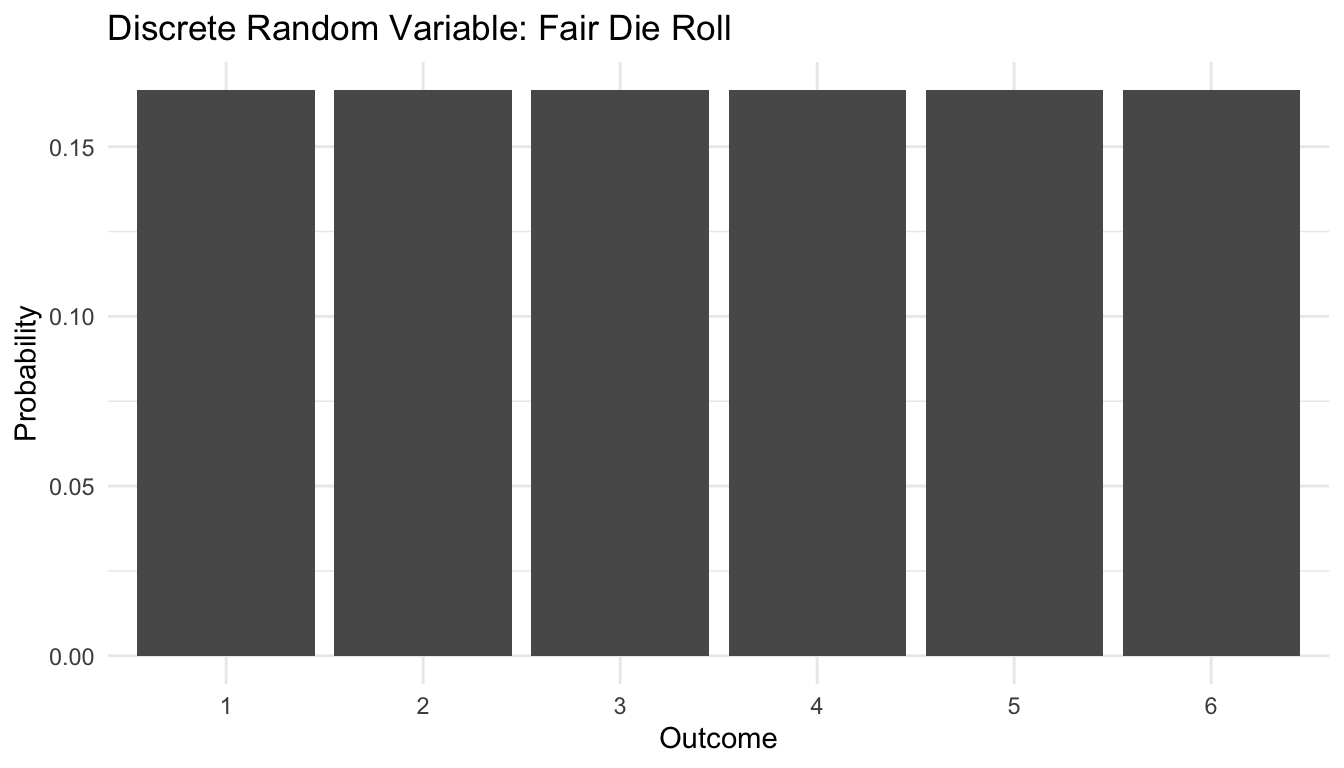

die_df# A tibble: 6 × 2

x prob

<int> <dbl>

1 1 0.167

2 2 0.167

3 3 0.167

4 4 0.167

5 5 0.167

6 6 0.167Random variables are often introduced early in probability, but their real importance becomes clearer much later.

They allow us to move from talking about uncertain events to talking about uncertain quantities.

Instead of asking only:

we begin asking:

This is where random variables become foundational for machine learning (DeGroot and Schervish 2012; Murphy 2012).

They support:

This also matters in trauma care and operational medicine.

A trauma system does not just face uncertain events. It faces uncertain quantities:

Those are all naturally represented as random variables.

Machine learning models do not optimize single outcomes. They optimize expected behavior across uncertain outcomes.

Probability begins with uncertain events.

Random variables go one step further.

A random variable assigns a numerical value to the outcome of a random process (DeGroot and Schervish 2012; Wasserman 2004).

For example:

This shift matters.

It lets us describe not just whether something happens, but how much happens.

That is essential in AI and ML, where models often predict quantities, probabilities, or losses rather than simple yes/no outcomes.

In practice, the random variable is the mathematical bridge between messy reality and a formal model.

For trauma clinicians and analysts, random variables are everywhere.

Examples include:

discrete random variables

continuous random variables

This framing matters because different clinical questions imply different kinds of statistical models.

If the variable is a count, a count model may be appropriate. If the variable is continuous, a Gaussian-type model may be a useful starting point. If the variable is binary, the random variable takes values like 0 and 1 and logistic-type models become relevant.

So before fitting any model, one of the first questions should be:

What is the random variable of interest?

Random variables generally fall into two broad classes.

A discrete random variable takes values from a countable set.

Examples include:

A die roll is the classic example.

library(tibble)

library(dplyr)

library(ggplot2)

die_df <- tibble::tibble(

x = 1:6,

prob = rep(1 / 6, 6)

)

die_df# A tibble: 6 × 2

x prob

<int> <dbl>

1 1 0.167

2 2 0.167

3 3 0.167

4 4 0.167

5 5 0.167

6 6 0.167The table above is a probability mass function for a discrete random variable. It tells us which values are possible and how much probability mass sits on each value.

ggplot2::ggplot(die_df, ggplot2::aes(x = factor(x), y = prob)) +

ggplot2::geom_col() +

ggplot2::labs(

title = "Discrete Random Variable: Fair Die Roll",

x = "Outcome",

y = "Probability"

) +

ggplot2::theme_minimal()

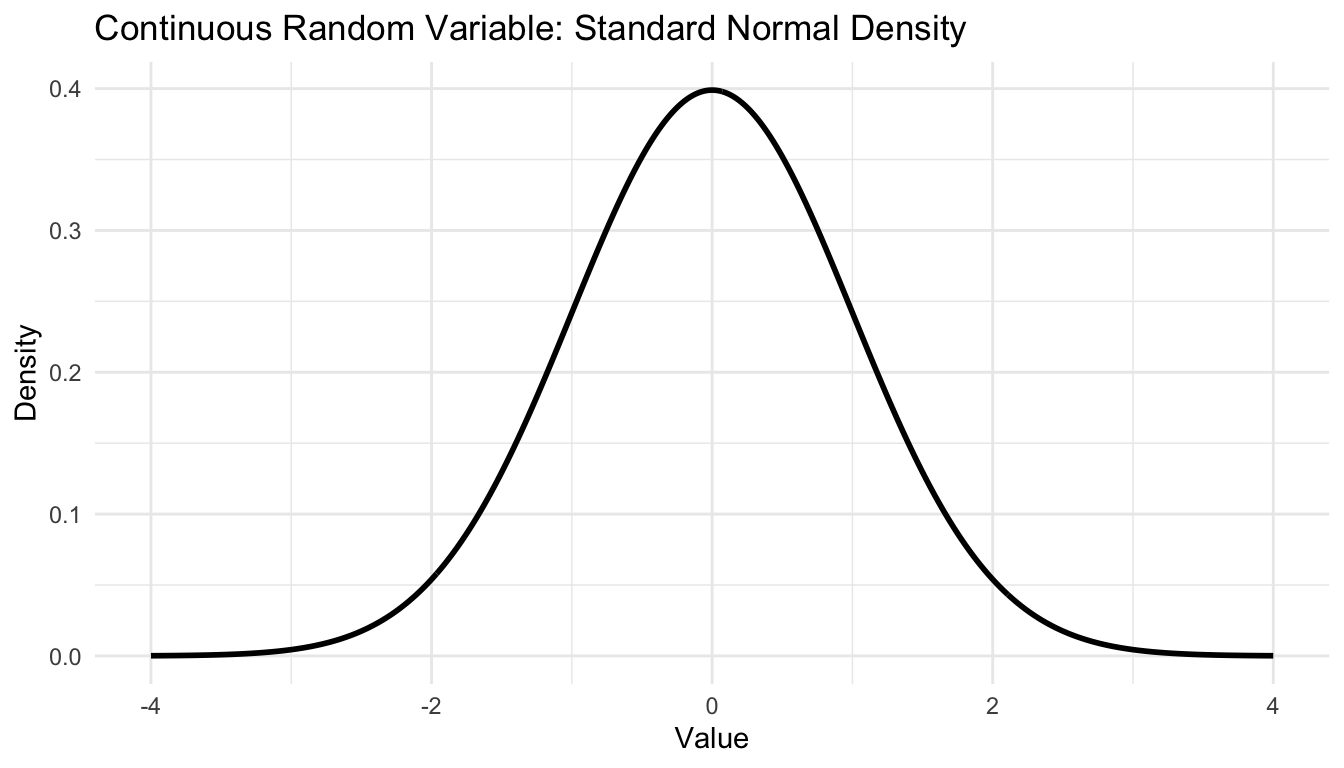

A continuous random variable can take values across an interval of real numbers.

Examples include:

For continuous variables, we talk about density, not point probability.

That distinction matters. For a continuous random variable, the probability of observing any exact single value is effectively zero. Instead, probability is assigned over intervals.

x_grid <- seq(-4, 4, length.out = 500)

norm_df <- tibble::tibble(

x = x_grid,

density = dnorm(x_grid, mean = 0, sd = 1)

)

ggplot2::ggplot(norm_df, ggplot2::aes(x = x, y = density)) +

ggplot2::geom_line(linewidth = 1) +

ggplot2::labs(

title = "Continuous Random Variable: Standard Normal Density",

x = "Value",

y = "Density"

) +

ggplot2::theme_minimal()

The distinction between discrete and continuous variables is not merely technical.

It affects how we calculate probabilities, expectations, and losses, and it strongly influences the modeling strategy we choose.

A random variable is meaningful only together with its distribution.

The distribution tells us:

For a discrete random variable, we often use a probability mass function.

For a continuous random variable, we often use a probability density function.

In machine learning, modelers often focus on predictions while forgetting that predictions are embedded in distributions.

But the distribution is the real object of interest whenever uncertainty matters (DeGroot and Schervish 2012; Murphy 2012).

A point prediction without a distributional mindset can hide important facts about:

The expectation or expected value of a random variable is its weighted average value under the distribution (DeGroot and Schervish 2012; Wasserman 2004).

For a discrete random variable:

\[ E[X] = \sum_x x P(X = x) \]

For a continuous random variable:

\[ E[X] = \int x f(x) \, dx \]

Expectation is often interpreted as the long-run average over repeated draws.

For a fair die roll:

expected_die <- sum(die_df$x * die_df$prob)

expected_die[1] 3.5The expected value is 3.5.

Of course, no individual roll of a die can produce 3.5.

That is the point.

Expectation is not a prediction of a single outcome. It is a summary of the distribution across repeated uncertainty.

This distinction is crucial in ML.

Expected loss, expected risk, and expected reward are population-level ideas, not guarantees for any single case.

Expectation is deeply practical.

A planner may ask:

These are expectation questions.

But expected value alone is never the whole story. Two scenarios can have the same expected blood demand but very different tail risk. One may be operationally manageable, while the other may produce occasional catastrophic shortages.

That is why expectation is useful, but insufficient by itself.

Expectation alone is not enough.

Two random variables can have the same expected value while behaving very differently.

Variance measures the spread around the mean (DeGroot and Schervish 2012):

\[ \mathrm{Var}(X) = E[(X - E[X])^2] \]

For the die example:

variance_die <- sum((die_df$x - expected_die)^2 * die_df$prob)

variance_die[1] 2.916667Variance matters because systems do not only care about average behavior.

They also care about stability, volatility, and risk.

A model with low average error but extremely high variability may be unreliable in deployment.

A medical logistics system with manageable average demand but large variance may still fail under surge conditions.

This is why both expectation and variance matter in applied decision-making.

Expectation and variance are examples of more general summary quantities called moments.

Moments help describe features such as:

The first moment is the mean.

The second central moment is the variance.

Higher moments often connect to skewness and kurtosis.

In practice, not every applied analyst needs to derive moments by hand, but understanding the idea is useful:

distributions are not just pictures; they can be summarized mathematically in ways that matter for prediction and uncertainty.

This is especially relevant in AI/ML because loss surfaces, residual structures, and predictive uncertainty often depend not just on average behavior, but on broader distributional shape.

One of the most useful properties in probability is linearity of expectation:

\[ E[X + Y] = E[X] + E[Y] \]

More generally,

\[ E[aX + bY] = aE[X] + bE[Y] \]

This holds whether or not the random variables are independent.

That last point is easy to overlook and extremely important.

It means we can compute expected totals without always needing the full joint distribution.

For example, suppose two games each pay random amounts.

game_df <- tibble::tibble(

outcome = c("Lose", "Win"),

payoff = c(-1, 3),

prob = c(0.7, 0.3)

)

expected_game <- sum(game_df$payoff * game_df$prob)

expected_two_games <- expected_game + expected_game

tibble::tibble(

quantity = c("E[Game 1]", "E[Game 2]", "E[Game 1 + Game 2]"),

value = c(expected_game, expected_game, expected_two_games)

)# A tibble: 3 × 2

quantity value

<chr> <dbl>

1 E[Game 1] 0.2

2 E[Game 2] 0.2

3 E[Game 1 + Game 2] 0.4This simple idea shows up everywhere:

In trauma systems, it can also apply to expected total blood demand across a set of incoming casualties or expected occupancy burden across a ward or ICU.

Gambling is often the simplest way to build intuition for expectation.

Suppose a game costs $2 to enter.

You roll one die:

What is the expected net payoff?

gamble_df <- tibble::tibble(

outcome = c("Roll 6", "Not 6"),

net_payoff = c(8, -2),

prob = c(1/6, 5/6)

)

expected_gamble <- sum(gamble_df$net_payoff * gamble_df$prob)

expected_gamble[1] -0.3333333Even when a game has a positive expected value, it may still involve substantial uncertainty.

That is why expectation is necessary but not sufficient.

In ML, this parallels the difference between:

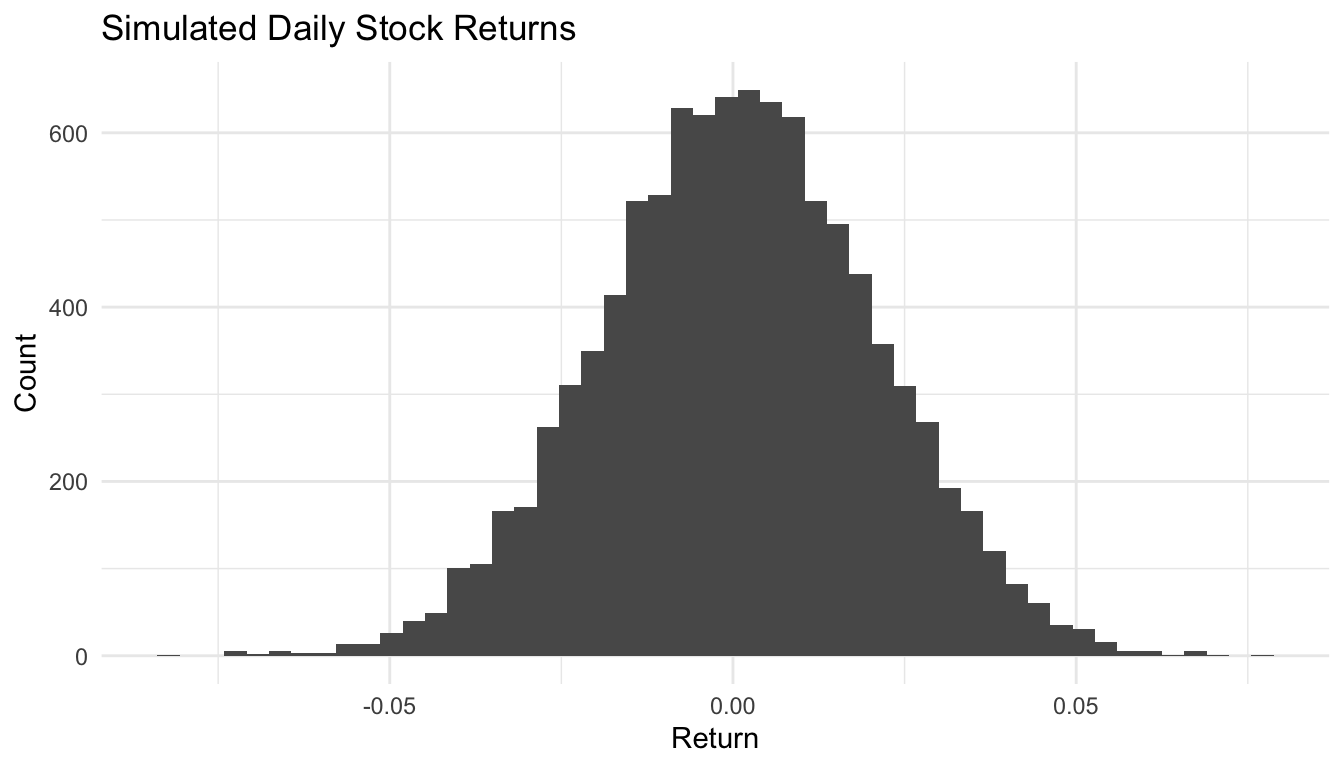

Financial returns are a familiar example of uncertain quantities.

Suppose a stock has daily returns modeled as approximately normal with:

We can simulate many possible one-day returns.

sim_returns <- tibble::tibble(

return = rnorm(10000, mean = 0.0005, sd = 0.02)

)

sim_returns |>

dplyr::summarise(

mean_return = mean(return),

var_return = var(return),

sd_return = sd(return)

)# A tibble: 1 × 3

mean_return var_return sd_return

<dbl> <dbl> <dbl>

1 0.000737 0.000400 0.0200ggplot2::ggplot(sim_returns, ggplot2::aes(x = return)) +

ggplot2::geom_histogram(bins = 50) +

ggplot2::labs(

title = "Simulated Daily Stock Returns",

x = "Return",

y = "Count"

) +

ggplot2::theme_minimal()

This example is useful because it illustrates several ideas at once:

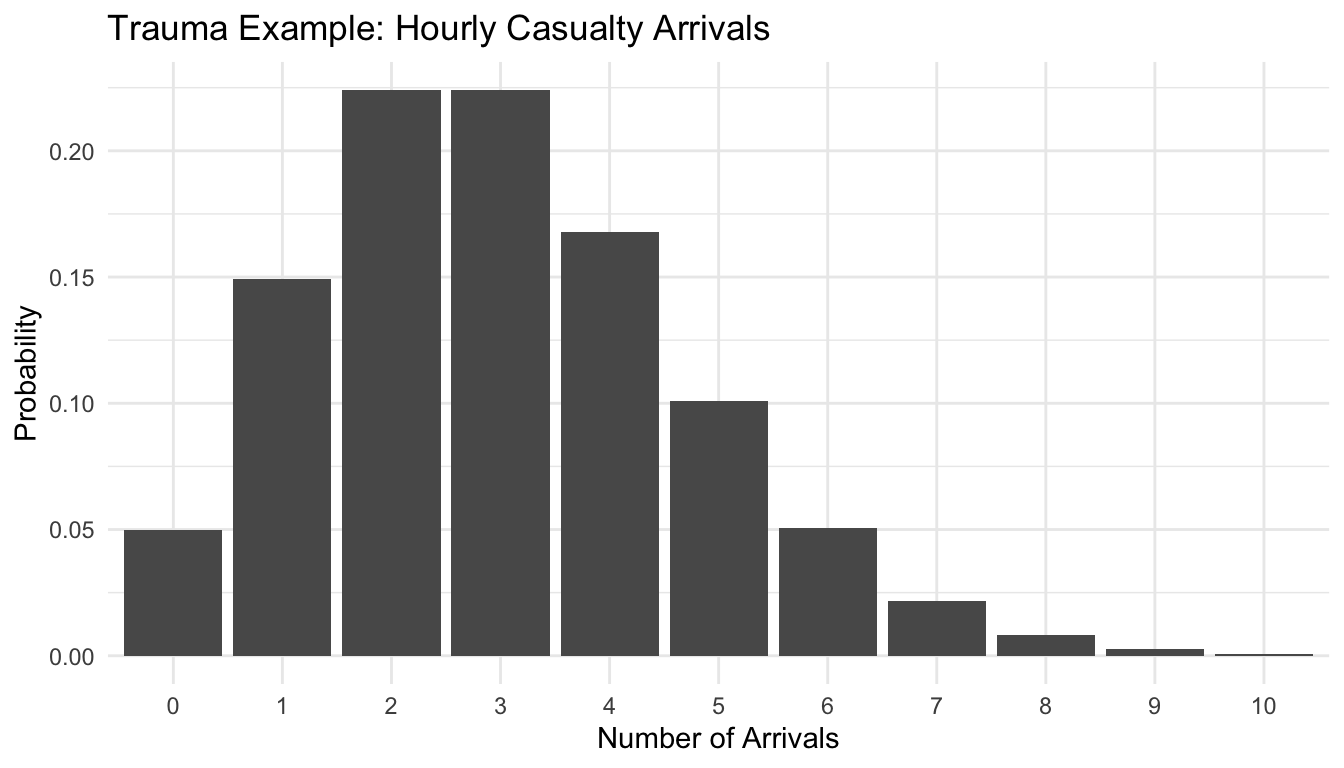

To connect this more directly to trauma operations, suppose the number of casualties arriving in one hour is modeled as a count random variable.

A common starting point for counts is the Poisson distribution.

Let:

\[ X = \text{number of casualty arrivals in one hour} \]

and suppose:

\[ X \sim \text{Poisson}(\lambda = 3) \]

Then the expected number of arrivals in an hour is 3.

arrival_df <- tibble::tibble(

x = 0:10,

prob = dpois(0:10, lambda = 3)

)

arrival_df# A tibble: 11 × 2

x prob

<int> <dbl>

1 0 0.0498

2 1 0.149

3 2 0.224

4 3 0.224

5 4 0.168

6 5 0.101

7 6 0.0504

8 7 0.0216

9 8 0.00810

10 9 0.00270

11 10 0.000810ggplot2::ggplot(arrival_df, ggplot2::aes(x = factor(x), y = prob)) +

ggplot2::geom_col() +

ggplot2::labs(

title = "Trauma Example: Hourly Casualty Arrivals",

x = "Number of Arrivals",

y = "Probability"

) +

ggplot2::theme_minimal()

Now compute the expected value and variance directly from the distribution.

expected_arrivals <- sum(arrival_df$x * arrival_df$prob)

variance_arrivals <- sum((arrival_df$x - expected_arrivals)^2 * arrival_df$prob)

tibble::tibble(

quantity = c("Expected arrivals", "Variance"),

value = c(expected_arrivals, variance_arrivals)

)# A tibble: 2 × 2

quantity value

<chr> <dbl>

1 Expected arrivals 3.00

2 Variance 2.98This kind of thinking can support:

One of the most important reasons random variables matter in ML is that learning is often framed as expected risk minimization (Murphy 2012).

Very loosely, the goal is to find a model \(f\) that minimizes the expected loss:

\[ R(f) = E[L(Y, f(X))] \]

where:

This equation is central.

It says the model is not judged on a single observation, but on its average loss across the distribution of possible data.

That is expectation doing the work.

In practice, empirical risk minimization approximates this expectation with sample averages.

But conceptually, the target is still expected loss under uncertainty.

This is one reason random variables are not optional background theory. They are embedded directly in how learning objectives are defined.

Even optimization methods like gradient descent are easier to understand once expectation enters the picture.

When training models, we often estimate gradients using samples or mini-batches.

These sample-based gradients can be viewed as noisy estimates of an underlying population gradient.

In other words, optimization often proceeds by using realized samples to approximate expected quantities.

This is one reason probabilistic thinking matters even in systems that are not explicitly Bayesian.

Randomness is not peripheral. It is built into the data-generating process, the objective function, and often the optimization itself (Murphy 2012).

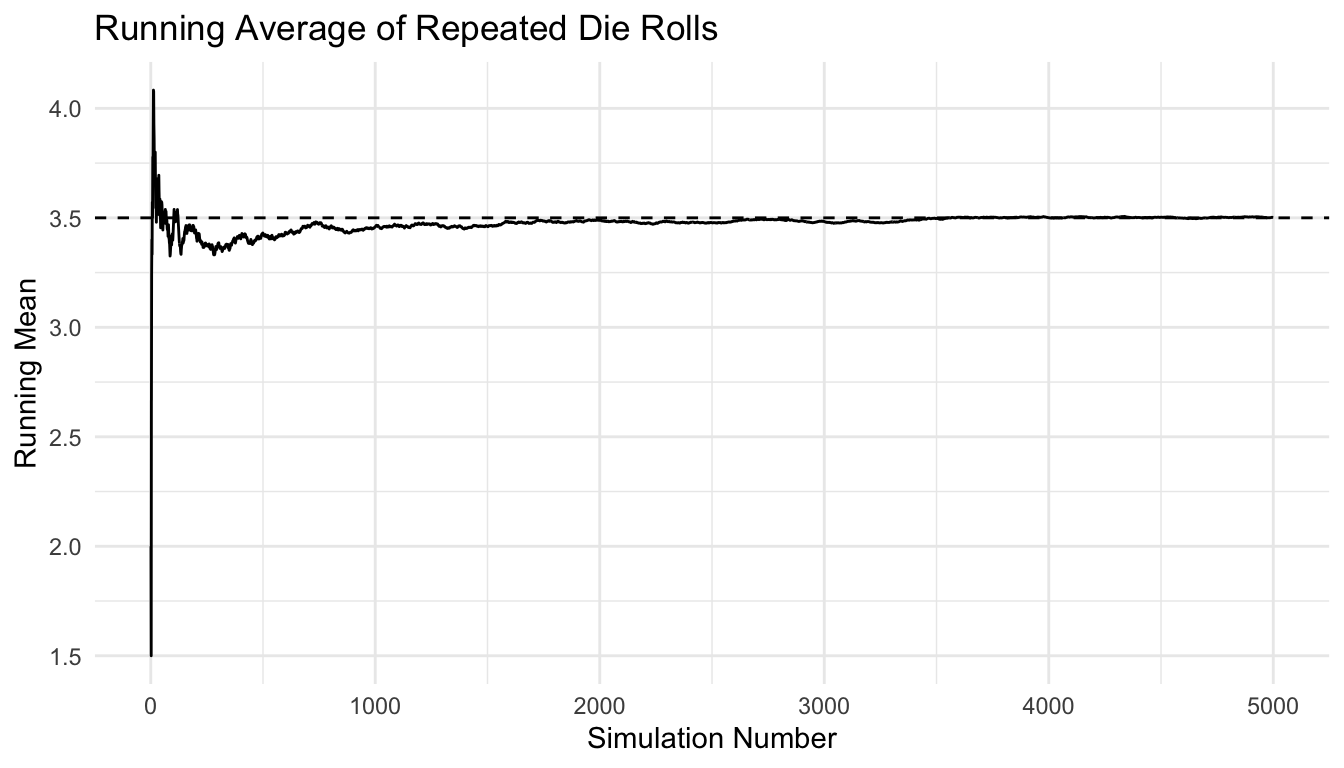

One of the best ways to teach random variables is to simulate repeated draws and watch the empirical behavior develop.

For example, here we repeatedly roll a die and track the running average.

n_sims <- 5000

sim_die <- tibble::tibble(

draw = 1:n_sims,

value = sample(1:6, n_sims, replace = TRUE)

) |>

dplyr::mutate(

running_mean = cumsum(value) / dplyr::row_number()

)

head(sim_die)# A tibble: 6 × 3

draw value running_mean

<int> <int> <dbl>

1 1 2 2

2 2 1 1.5

3 3 5 2.67

4 4 5 3.25

5 5 4 3.4

6 6 3 3.33ggplot2::ggplot(sim_die, ggplot2::aes(x = draw, y = running_mean)) +

ggplot2::geom_line(linewidth = 0.5) +

ggplot2::geom_hline(yintercept = expected_die, linetype = 2) +

ggplot2::labs(

title = "Running Average of Repeated Die Rolls",

x = "Simulation Number",

y = "Running Mean"

) +

ggplot2::theme_minimal()

This makes the abstract idea of expectation more concrete. The expected value is not the outcome of one draw. It is the value toward which the long-run average tends to stabilize.

That idea sits behind many simulation methods in AI, ML, and operations research.

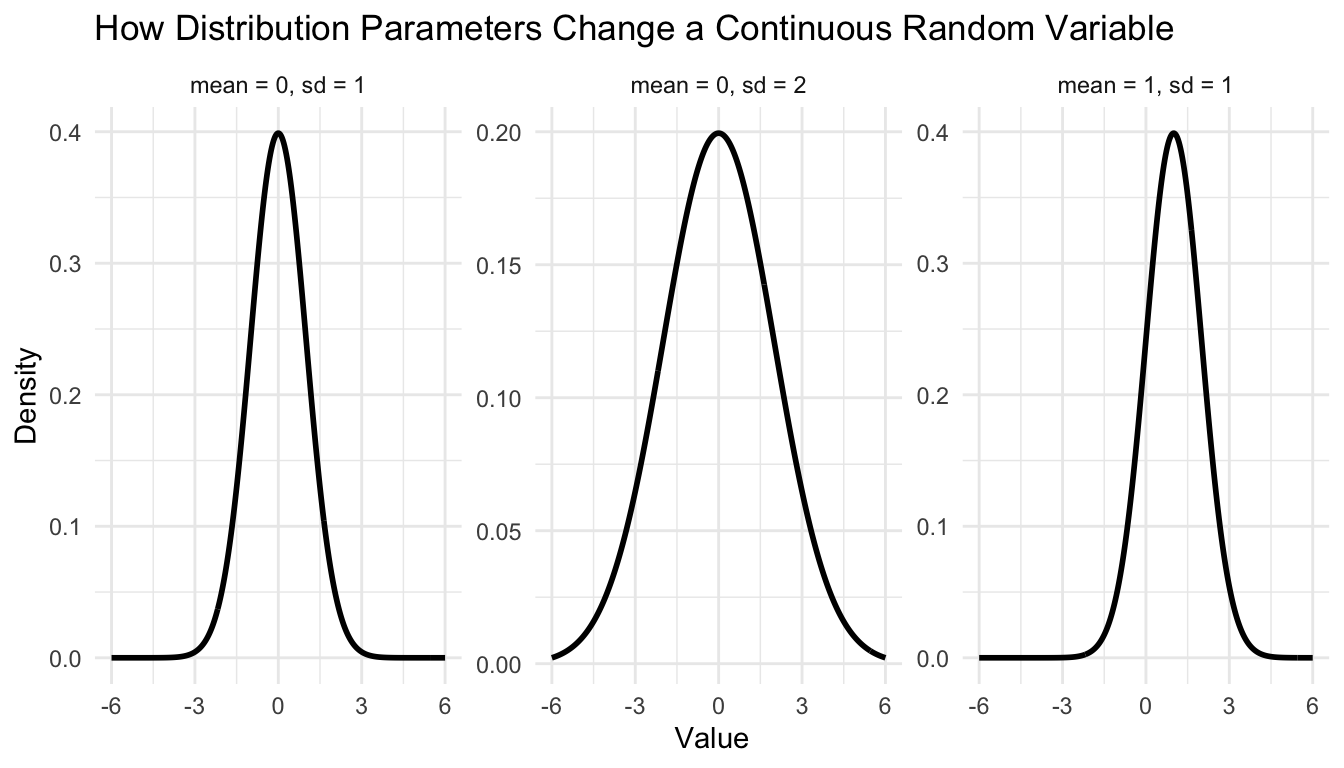

One of the best ways to teach random variables is to visualize how distributions change as parameters change.

For example, here is a simple illustration using normal densities with different means and standard deviations.

param_df <- tibble::tribble(

~mean, ~sd, ~label,

0, 1, "mean = 0, sd = 1",

1, 1, "mean = 1, sd = 1",

0, 2, "mean = 0, sd = 2"

)

plot_df <- param_df |>

dplyr::rowwise() |>

dplyr::do(

tibble::tibble(

x = seq(-6, 6, length.out = 400),

density = dnorm(seq(-6, 6, length.out = 400), mean = .$mean, sd = .$sd),

label = .$label

)

) |>

dplyr::ungroup()

ggplot2::ggplot(plot_df, ggplot2::aes(x = x, y = density)) +

ggplot2::geom_line(linewidth = 1) +

ggplot2::facet_wrap(~ label, scales = "free_y") +

ggplot2::labs(

title = "How Distribution Parameters Change a Continuous Random Variable",

x = "Value",

y = "Density"

) +

ggplot2::theme_minimal()

In a fuller Quarto website workflow, you could make these truly interactive with plotly, html widgets, or Shiny components.

But even static visuals go a long way toward making the ideas less abstract.

Random variables are not just a technical definition.

They are the bridge between:

Without random variables, we cannot define:

They are not background machinery. They are part of the conceptual engine.

Before using a model or stochastic system, ask:

These questions sharpen both modeling and interpretation.

Every output of a clinical prediction model — a mortality probability, a readmission risk score, a triage acuity classification — is a realization of a random variable with a full distribution, not a fixed number; the model’s softmax output represents E[Y | X], the expected value of the outcome given features, and treating it as a deterministic answer rather than a distribution summary discards the variance information that determines whether any individual prediction should be acted on. In trauma triage systems deployed at Role 2 and Role 3 facilities, reporting a point estimate of 0.73 mortality risk without communicating prediction variance means two patients with the same score but very different uncertainty levels receive identical resource allocation — a clinically consequential error that the random-variable framing would prevent.

Random variables allow us to treat uncertainty as something measurable.

Expectation gives us a way to summarize long-run average behavior. Variance tells us how much uncertainty remains. Moments reveal additional structure. Linearity of expectation makes complex systems tractable.

In machine learning, these are not ornamental ideas.

They explain why loss functions work, why optimization behaves the way it does, and why predictions must be understood as summaries of uncertainty rather than deterministic truths.

In trauma analytics, they help frame operational questions rigorously:

Random variables are not just mathematical abstractions. They are how models translate uncertainty into prediction, risk, and action.

This post is part of the Prediction Modeling Toolkit — a companion reference with feature engineering templates, distribution diagnostics, and simulation-based modeling scaffolds.

This post is part of a broader Applied Statistics for AI and Clinical Decision-Making Series: